Interest rates determine the cost of borrowing and shape everything from mortgage payments to car-loan EMIs. When applying for a loan you’ll usually have two options: a fixed interest rate, which stays the same for the entire term, or a floating (variable) interest rate, which moves up or down with a market benchmark such as the RBI repo rate or a bank’s prime lending rate. Knowing how each option works—and its trade-offs—helps you pick the loan structure that fits your budget and risk comfort.

What Are Fixed and Floating Interest Rates?

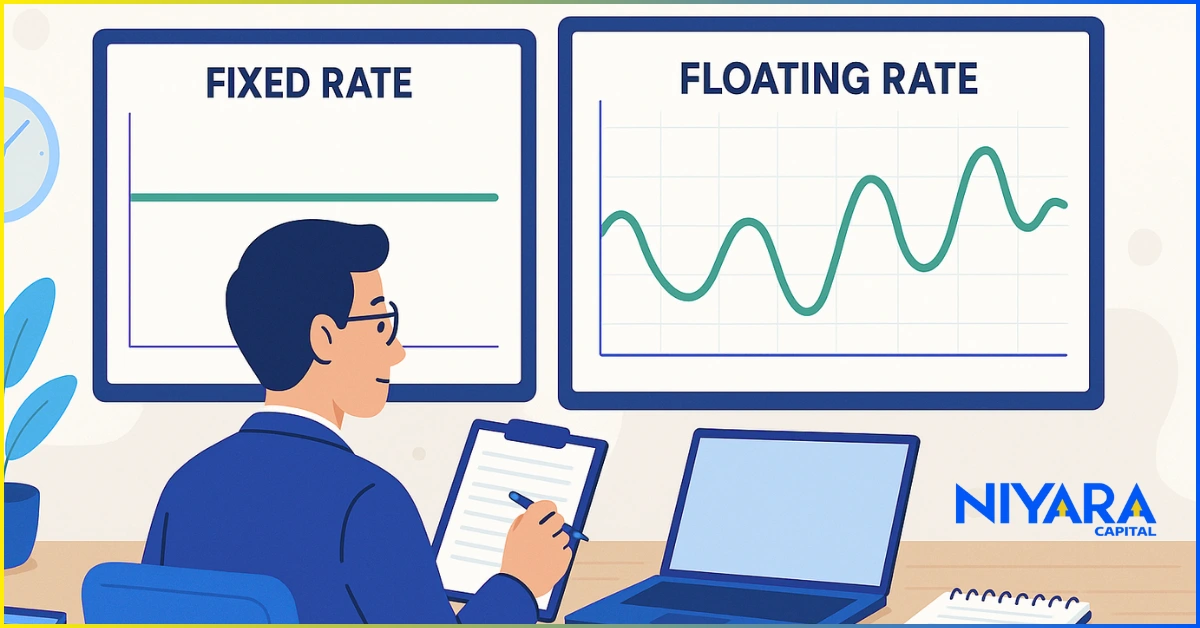

Fixed interest rate

Once your lender locks in a fixed rate, it never changes—even if market rates later rise or fall. Your monthly instalment (EMI) therefore remains identical from the first payment to the last.

Floating (variable) interest rate

A floating rate is tied to an external benchmark (for example, the RBI repo rate). Your EMI is recalculated at set intervals—often every three or six months—so it can decrease when rates fall and increase when they rise. Since October 2019, RBI rules require most new retail loans in India to be linked to an external benchmark, making floating-rate products common in home, education and personal loans.

Pros of Fixed Interest Rates

- Predictable payments

The EMI never changes, making monthly budgeting straightforward and stress-free. You always know the exact amount due.

- Protection from future hikes

If the central bank raises policy rates, fixed-rate borrowers are insulated. Your repayment schedule stays intact even in a high-inflation environment.

- Helpful in low-rate periods

When overall rates are already low, locking them in can save money over the loan’s life because you avoid potential upward swings.

Cons of Fixed Interest Rates

- Slightly higher starting rate

Lenders charge a premium for the certainty they provide, so initial fixed rates are often 1–2 percentage points higher than comparable floating rates.

- No automatic benefit from rate cuts

If market rates fall after you lock in, you’ll keep paying the older, higher rate unless you refinance—a process that involves time, paperwork and fees.

- Opportunity cost during prolonged downturns

In a declining-rate cycle, sticking with a fixed rate can mean paying more interest overall than a variable-rate borrower.

Pros of Floating Interest Rates

- Lower initial cost

Floating loans usually start below fixed-rate equivalents. The early EMI is cheaper, easing short-term cash-flow pressure.

- Automatic savings when rates fall

Because the interest resets with the benchmark, EMIs drop when policy rates are cut—no refinance required.

- Good fit for short-term or prepayment plans

If you expect to repay the loan quickly, you benefit from the lower initial rate without holding the risk for long.

Cons of Floating Interest Rates

- Payment uncertainty

Your EMI can rise without warning if benchmark rates climb, complicating household budgeting.

- Harder long-term planning

Because total interest payable is unknown, it’s tougher to forecast future cash-flow needs, especially on long-tenure loans.

- Potentially higher lifetime cost

In an extended rising-rate cycle, a floating loan can end up more expensive than a fixed one.

Choosing Between Fixed and Floating

| Factor | When a Fixed Rate Makes Sense | When a Floating Rate Makes Sense |

| Rate outlook | Economists expect rates to rise. | Rates are expected to fall or stay flat. |

| Budget stability | You need precise, unchanging monthly outflows. | Your income can handle EMI fluctuations. |

| Loan tenure | Short to Medium term loans (e.g., 5- 10 year tenures). | Long -term loans (e.g. 10 to 30 year loan tenures) |

| Risk tolerance | You prefer certainty, even at a slightly higher cost. | You’re comfortable trading certainty for potential savings. |

Tip: Ask your lender about (a) the external benchmark they use, (b) how often the rate resets, and (c) fees for switching between fixed and floating later. Understanding these details prevents surprises.

Conclusion

Fixed and floating interest rates each offer clear strengths:

- Fixed rates deliver stability and protect against future hikes but start higher and skip savings when rates fall.

- Floating rates begin cheaper and pass through rate cuts yet expose you to payment volatility.

Match the loan type to your personal circumstances—income stability, repayment horizon and risk appetite—to avoid unnecessary financial strain.

Sources

https://www.investopedia.com

https://www.rbi.org.in

https://krishijagran.com

Disclaimer

The information above is for general educational purposes and does not constitute financial, investment, tax or legal advice. Always consult a certified financial adviser or your lending institution before making borrowing decisions. Neither the author nor Niyara Capital Solutions is responsible for any loss arising from the use of this information.